believes it has room to grow its business")

Even when a company is making losses, it is possible for shareholders to make a profit if they buy a good company at an appropriate price. For example, Amazon.com lost money for years after going public, but if you had bought and held the stock since 1999, you could have made a lot of money. That being said, there are risks involved, as unprofitable companies can burn through all their cash and go into distress.

So the obvious question is, Ovid Therapeutics (NASDAQ:OVID) shareholders are debating whether they should be concerned about its cash burn rate. In this article, cash burn refers to the annual rate at which an unprofitable company spends cash to fund growth. Free cash flow is negative. First, compare its cash burn to its cash reserves to determine its cash runway.

Check out our latest analysis for Ovid Therapeutics.

What is Ovid Therapeutics' funding runway?

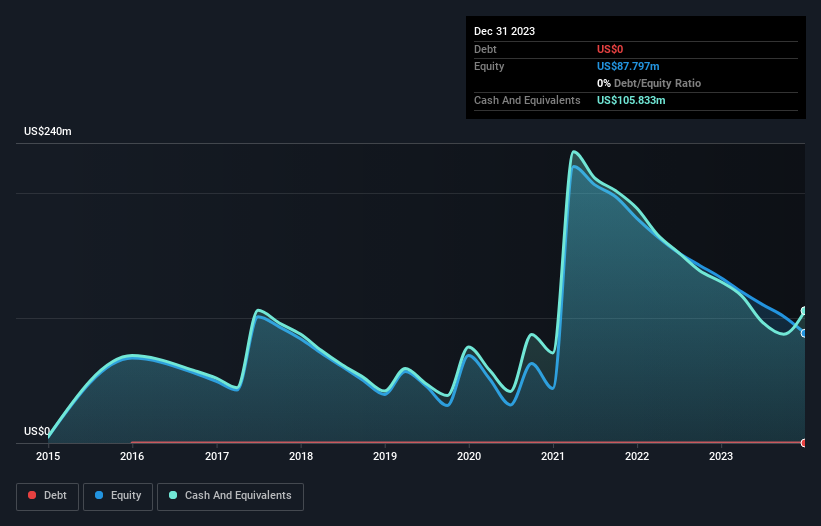

A company's cash runway can be calculated by dividing the amount of cash it holds by the rate at which it spends that cash. When Orvid Therapeutics last reported its December 2023 balance sheet in March 2024, it had zero debt and cash worth US$106m. Importantly, his cash burn in the trailing twelve months was US$46m. So it had a cash runway of 2.3 years starting December 2023. That's a reasonable number considering it takes the company several years to develop its business. You can see how its cash holdings have changed over time, as shown below.

How has Ovid Therapeutics' cash burn changed over time?

In our view, Ovid Therapeutics hasn't yet generated significant operating revenue, as it only reported US$392k in the last twelve months. As a result, we think it's premature to focus on revenue growth, and will limit ourselves to looking at how cash burn has changed over time. Coincidentally, the company's cash burn has decreased by 19% over the last year. This suggests that management has maintained a fairly stable business development rate despite a slight decline in spending. The past is always worth studying, but it is the future that matters most. For this reason, it makes a lot of sense to see what analysts are predicting for the company.

How difficult will it be for Ovid Therapeutics to raise more capital for growth?

Although its cash burn has been lower recently, shareholders should still consider how easy it will be for Orvid Therapeutics to raise more cash in the future. The most common ways for publicly traded companies to raise more money for their operations is by issuing new shares or taking on debt. Companies typically sell their new stock to raise cash and fuel growth. You can compare a company's cash burn to its market capitalization to find out how many new shares a company needs to issue to finance its operations for one year.

Orvid Therapeutics' cash burn of $46 million represents about 20% of its market capitalization of $224 million. This is not insignificant, and if the company had to sell enough shares to fund next year's growth at its current share price, it would likely witness significant and costly dilution. You'll probably end up doing it.

Are you worried about Ovid Therapeutics' cash burn?

In this analysis of Ovid Therapeutics' cash burn, we consider its cash runway to be reassuring, but we're a bit worried about its cash burn relative to its market capitalization. Cash burn companies are always on the risk side of things, but after considering all the factors we've discussed in this short article, we're not too worried about their cash burn rate. On a different note, Ovid Therapeutics two warning signs (and 1 is a concern) I think you should know.

of course, You may find a great investment if you look elsewhere. So take a look at this free List of interesting companies and this list of growth stocks (according to analyst forecasts)

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.